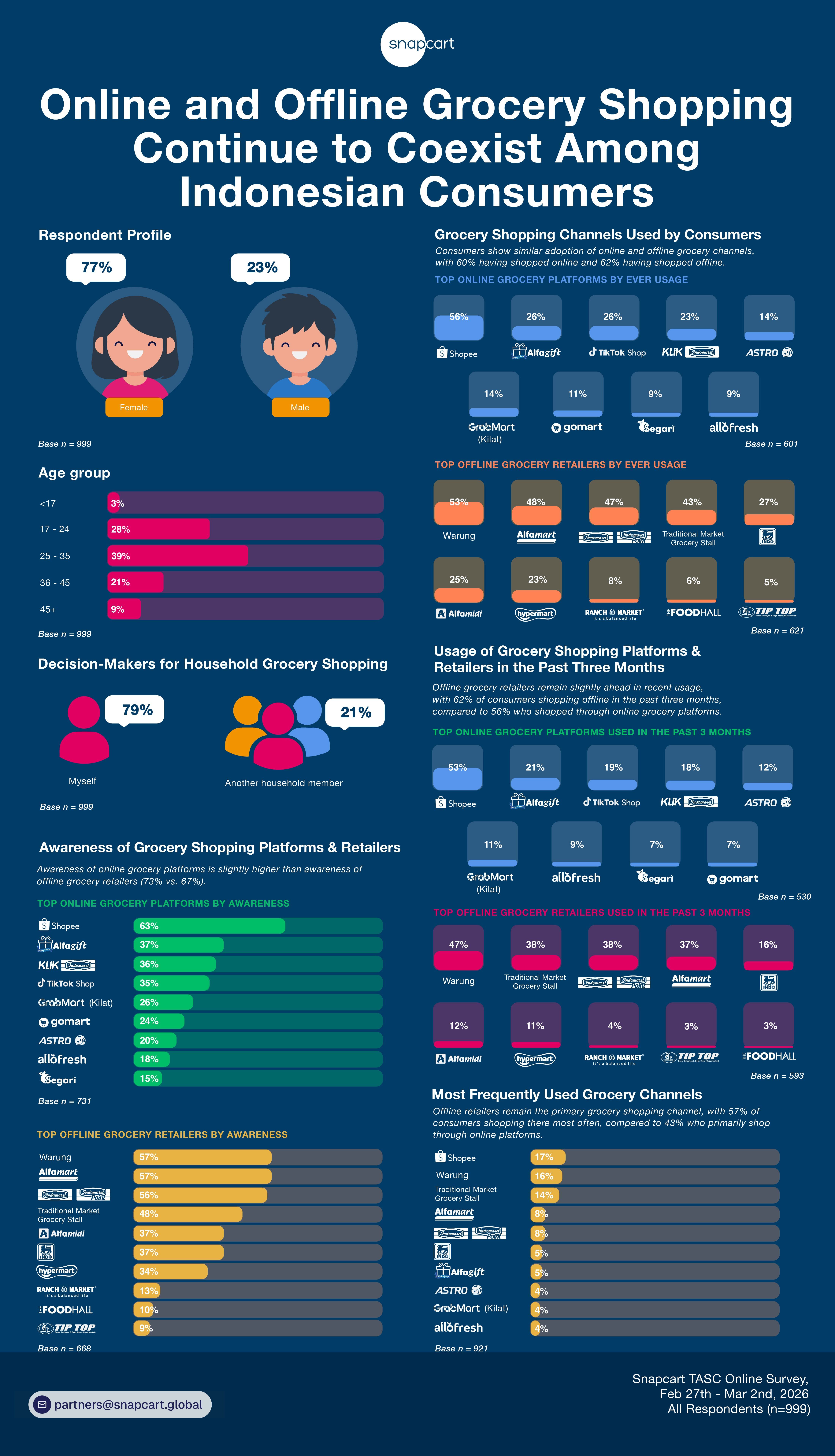

Grocery shopping remains an essential part of everyday life, and Indonesian consumers continue to utilize both online and offline channels to fulfill their household needs. To better understand grocery shopping behavior, Snapcart conducted an online survey involving 999 respondents across Indonesia, exploring awareness, usage, recent purchasing behavior, and preferred grocery shopping channels.

Consumers Take the Lead in Grocery Shopping Decisions

Household grocery shopping decisions are largely self-driven. Nearly eight in ten consumers (79%) reported that they personally decide where to shop for groceries, while only 21% rely on another household member to make the decision. This suggests that grocery retailers and platforms have significant opportunities to directly influence shoppers through pricing, promotions, convenience, and customer experience.

Awareness of Online Grocery Platforms Slightly Exceeds Offline Retailers

When asked which grocery shopping platforms or retailers they know, awareness of online grocery platforms was slightly higher than awareness of offline grocery retailers (73% vs. 67%).

Among online grocery platforms, Shopee emerged as the most recognized platform, with 63% awareness. It was followed by Alfagift (37%), Klik Indomaret (36%), and TikTok Shop (35%).

For offline grocery retailers, Warung and Alfamart shared the highest awareness level at 57%, closely followed by Indomaret (56%). Traditional market grocery stalls were recognized by nearly half of consumers (48%), while modern supermarket chains such as Alfamidi and Superindo each achieved 37% awareness.

Consumers Continue to Shop Across Both Online and Offline Channels

Usage data indicates that consumers actively shop through both channels. Sixty percent of respondents reported having purchased groceries through online platforms, while 62% had shopped at offline grocery retailers.

Shopee leads online grocery shopping adoption, with 56% of consumers having used the platform for grocery purchases. Alfagift and TikTok Shop followed at 26% each, while Klik Indomaret reached 23%.

Meanwhile, offline grocery shopping remains deeply rooted in daily routines. Warung (53%), Alfamart (48%), and Indomaret (47%) ranked as the most commonly used grocery shopping destinations. Traditional market grocery stalls also maintained strong relevance, attracting 43% of consumers.

Offline Retailers Maintain a Slight Advantage in Recent Grocery Purchases

Looking specifically at shopping activity during the past three months, offline grocery retailers continue to hold a modest lead over online channels. Sixty-two percent of consumers reported purchasing groceries from offline retailers during the period, compared with 56% who shopped through online grocery platforms.

Among online platforms, Shopee remained the dominant player, used by 53% of consumers in the past three months. Alfagift (21%), TikTok Shop (19%), and Klik Indomaret (18%) followed behind. For offline retailers, Warung continued to lead recent grocery purchases at 47%, while Indomaret and traditional market grocery stalls each reached 38%, closely followed by Alfamart at 37%.

Online Grocery Platforms in the Past Three Months

Shopee dominates online grocery shopping across Indonesia. The platform consistently records the highest usage across all regions, exceeding 50% in major markets such as South Sumatra (64%), East Java (59%), and Kalimantan (57%). This strong performance suggests that Shopee has successfully established itself as the leading destination for online grocery purchases nationwide. Notably, Shopee’s adoption remains strong across all socioeconomic groups, reaching 67% among SES DE consumers, highlighting its broad appeal across different income segments.

Modern retail platforms are emerging as strong challengers. Supported by their extensive offline store networks, Alfagift and Klik Indomaret have built a broad regional presence. Alfagift performs particularly well in Central Java + DIY (34%), while Klik Indomaret reaches nearly three in ten consumers in North Sumatra (29%), demonstrating the advantage of combining physical retail reach with digital convenience.

TikTok Shop performs best in highly populated regions. The platform records its strongest grocery penetration in West Java (26%) and Central Java + DIY (25%), suggesting that its appeal is particularly strong among digitally engaged consumers in densely populated markets. TikTok Shop also shows stronger adoption among middle and lower-income consumers, reaching 23% among SES B consumers and 27% among SES DE consumers, compared with 13% among SES A consumers.

Quick-commerce players remain concentrated in metropolitan areas. Astro leads the grocery-specialized platform segment with 25% penetration in DKI Jakarta, significantly outperforming other quick-commerce players. However, its presence remains considerably lower outside the capital, indicating that rapid-delivery grocery services have yet to achieve nationwide scale. Similar patterns can be seen across socioeconomic groups, where Astro and GrabMart tend to attract higher-income consumers, reflecting the premium positioning often associated with on-demand grocery delivery services.

Offline Groceries Platforms in the Past Three Months

Warung remains the backbone of grocery shopping across Indonesia. The channel consistently records the highest usage across multiple regions, reaching 61% in Central Sumatra and 60% in Central Java + DIY. These results reinforce the enduring importance of neighborhood stores for routine and small-quantity grocery purchases.

The role of traditional trade is particularly pronounced among lower-income consumers. The role of traditional trade is particularly pronounced among lower-income consumers. Warung reaches 58% penetration among SES DE consumers and 54% among SES C consumers, compared with 36% among SES A consumers. This suggests that affordability, accessibility, and habitual shopping behavior continue to make traditional trade an important channel for daily grocery needs.

Modern minimarkets continue to strengthen their role in daily shopping. Indomaret records particularly high usage in Kalimantan (67%), and Banten (53%), Alfamart performs strongly in Sulawesi (50%), and West Java (46%), reinforcing their position as convenient neighborhood shopping destinations. Modern retail formats also tend to attract higher-income consumers, with Alfamart reaching 44% among SES A and SES B consumers.

Traditional market stalls remain highly relevant. Traditional market grocery stalls continue to attract a substantial share of consumers, particularly in Central Sumatra (61%), Kalimantan (48%), and Central Java + DIY (47%). This demonstrates that traditional trade remains deeply embedded in consumers’ grocery shopping habits, especially for staple and fresh food purchases.

Supermarkets serve more planned shopping occasions. Compared to traditional trade and minimarkets, supermarkets and premium grocery stores such as Super Indo, Hypermart, Ranch Market, and Foodhall record significantly lower penetration, suggesting they are more commonly used for planned or bulk shopping missions rather than routine purchases. Their usage is also more concentrated among higher-income consumers, with Superindo reaching 24% penetration among SES A consumers compared to just 11% among SES C and DE consumers.

Overall, the findings highlight that while online grocery shopping has become increasingly mainstream, Indonesia’s grocery landscape remains heavily influenced by traditional trade and convenience-driven retail formats. Consumers continue to embrace both channels, but offline retailers remain the primary destination for everyday grocery needs.

Offline Channels Remain the Preferred Grocery Shopping Destination

Although consumers engage with both online and offline channels, offline retailers continue to be the preferred destination for regular grocery shopping. When asked where they shop most often for groceries, 57% selected offline retailers, compared with 43% who primarily shop through online platforms. Among individual retailers, Shopee ranked as the most frequently used grocery shopping destination (17%), followed by Warung (16%), traditional market grocery stalls (14%), and both Alfamart and Indomaret (8% each).

The findings highlight that Indonesian consumers are increasingly embracing digital grocery shopping options while maintaining strong reliance on traditional retail formats. Rather than replacing offline shopping, online grocery platforms appear to complement existing shopping habits, creating an omnichannel grocery landscape where consumers freely move between digital and physical retail channels depending on their needs and preferences.

Key Insights

1. Grocery Shopping Decisions Are Highly Individual

Nearly eight in ten consumers (79%) personally decide where to shop for groceries, making individual shoppers the primary target for retailers and brands seeking to influence purchase decisions.

2. Online Grocery Shopping Has Become Mainstream

With 60% of consumers having purchased groceries online and awareness surpassing offline retailers, digital grocery shopping has become an established part of everyday consumer behavior.

3. Shopee Leads While Retail-Owned Platforms Strengthen Their Presence

Shopee remains the clear leader across awareness, usage, and recent purchases, while Alfagift and Klik Indomaret demonstrate how established retail networks can successfully compete in the digital grocery space.

4. Traditional Trade Remains the Foundation of Offline Grocery Shopping

Warung and traditional market stalls continue to play a central role in consumers’ grocery purchases, particularly among lower-income households, highlighting the enduring importance of accessibility, affordability, and habitual shopping behavior.

5. Quick-Commerce Remains an Urban and Affluent Consumer Play

While grocery-specialized platforms perform strongly in metropolitan markets, their penetration remains concentrated among urban and higher-income consumers, suggesting that rapid-delivery grocery services have yet to achieve mass-market adoption nationwide.

6. Offline Retailers Remain the Preferred Grocery Shopping Channel

Consumers actively engage with both online and offline channels, but offline retailers remain the preferred destination for routine grocery purchases, indicating that digital platforms are complementing rather than replacing traditional shopping habits.

Need to learn more about consumer habits and behavior? Contact us at partners@snapcart.global