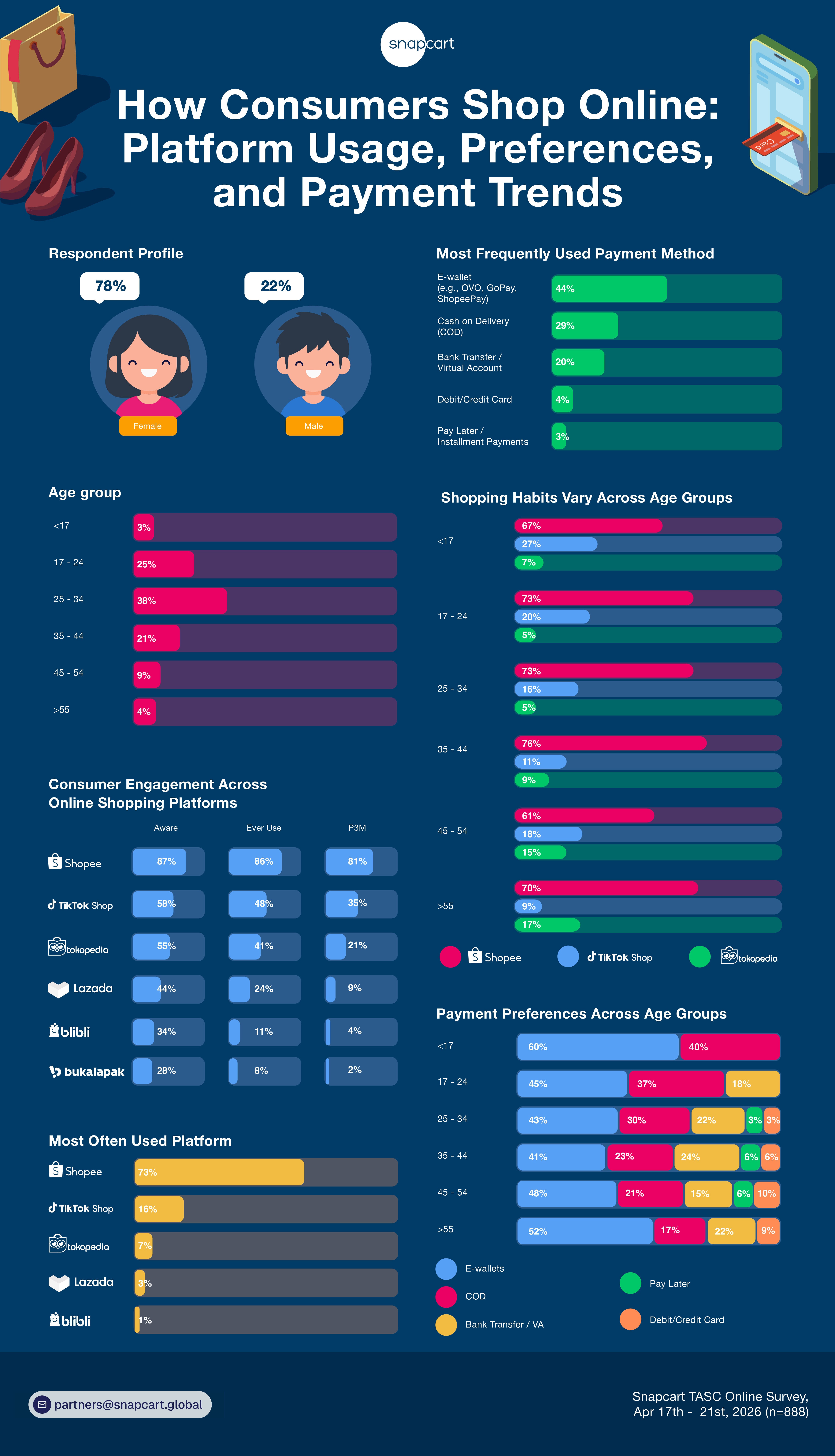

Online shopping has become an integral part of daily life for many Indonesians. To better understand how consumers engage with e-commerce platforms, a survey of 888 respondents explored platform awareness, usage behavior, shopping preferences, and payment methods. The findings reveal a highly competitive market where consumers are familiar with multiple platforms, yet a small number of players capture the majority of shopping activity.

Awareness Does Not Always Translate into Active Usage

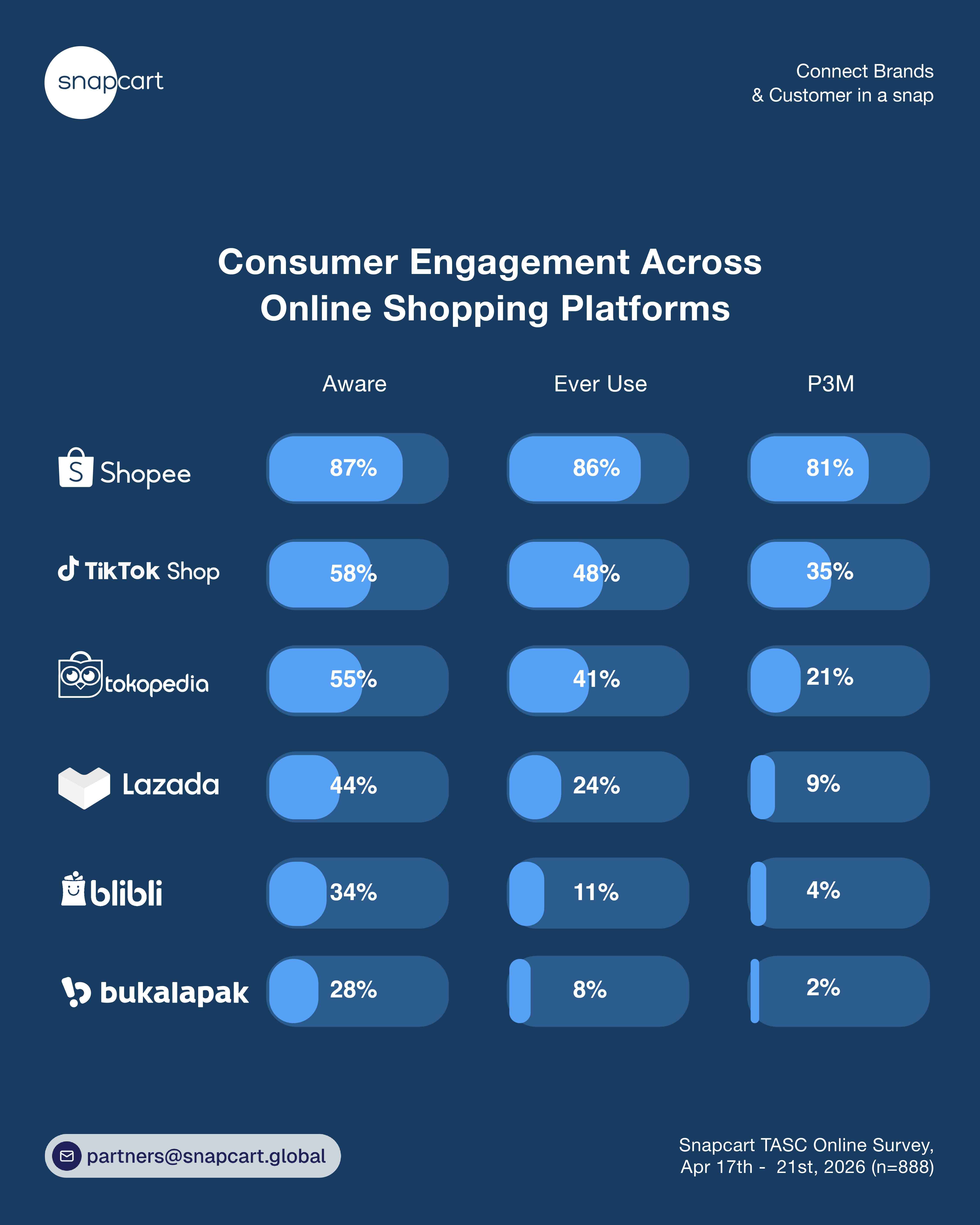

The survey shows that awareness of e-commerce platforms is widespread among Indonesian consumers. Shopee leads in overall awareness (87%), followed by TikTok Shop (58%) and Tokopedia (55%). Lazada (44%), Blibli (34%), and Bukalapak (28%) trail behind. However, awareness alone does not guarantee sustained engagement. When comparing awareness with actual usage, significant differences emerge across platforms.

The result suggests that consumers may be aware of several marketplaces, but only a subset successfully maintains regular engagement. Platforms that are able to convert awareness into active usage appear to have a stronger position in consumers’ shopping routines.

Consumers Tend to Consolidate Their Shopping Activities

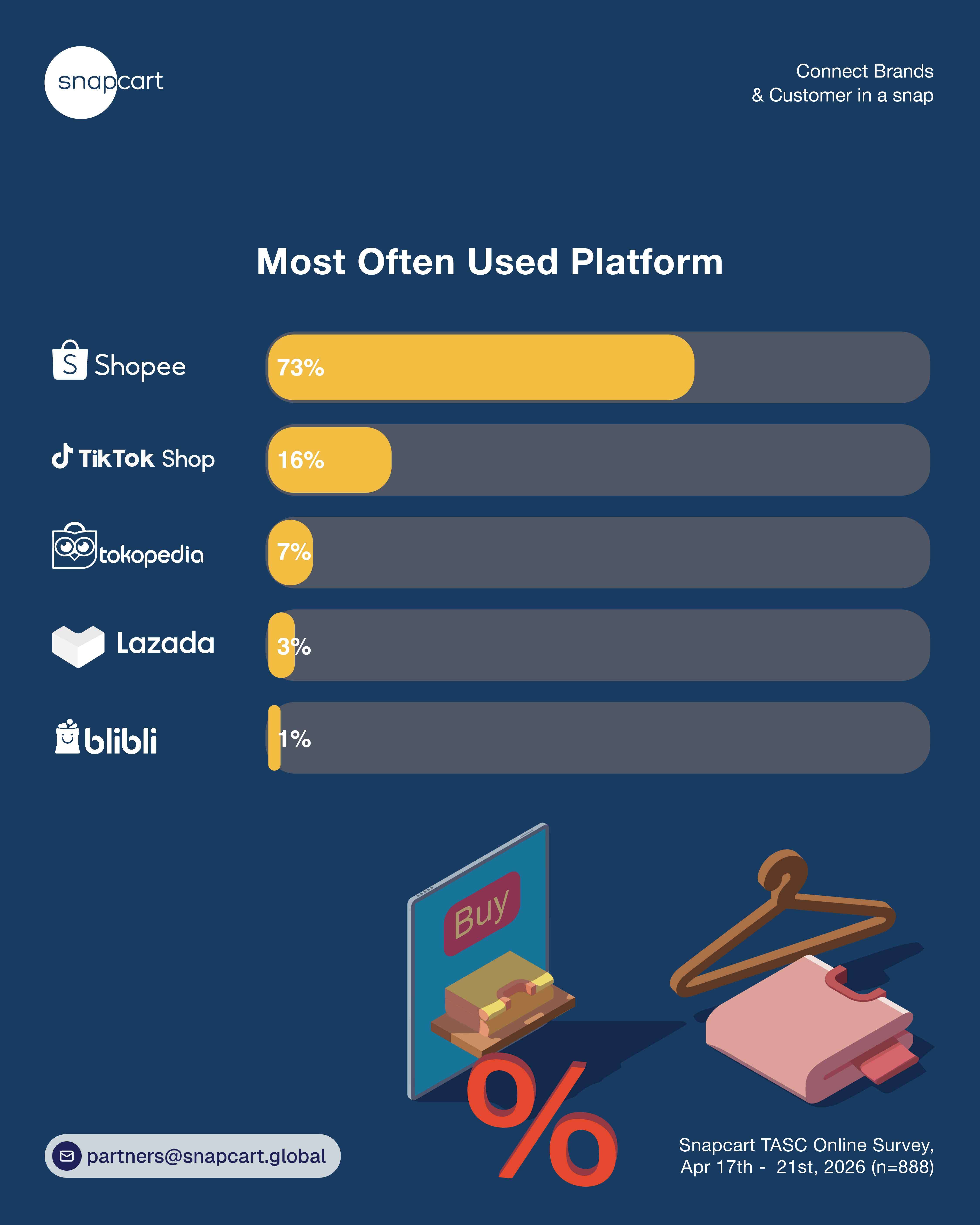

One of the most notable findings is the gap between multi-platform usage and primary platform preference. While many respondents have experience using multiple marketplaces, most eventually concentrate their shopping activity on a single platform. When asked which platform they use most frequently, nearly three-quarters of online shoppers selected Shopee.

This indicates that although consumers often browse across different marketplaces, convenience, pricing, promotions, logistics, and familiarity ultimately drive them toward a preferred platform for repeat purchases. The findings suggest that winning consumer attention is no longer enough. The bigger challenge for platforms is becoming consumers’ default shopping destination.

TikTok Shop Continues to Strengthen Its Position

Among all competitors, TikTok Shop appears to have established itself as the strongest alternative platform. Nearly half of respondents (48%) have used TikTok Shop, while 35% reported using it within the last three months. Furthermore, 16% identified TikTok Shop as their most frequently used platform. These figures highlight the growing role of content-driven commerce in Indonesia. The integration of entertainment, product discovery, and purchasing within a single ecosystem may be helping TikTok Shop remain relevant in consumers’ shopping journeys.

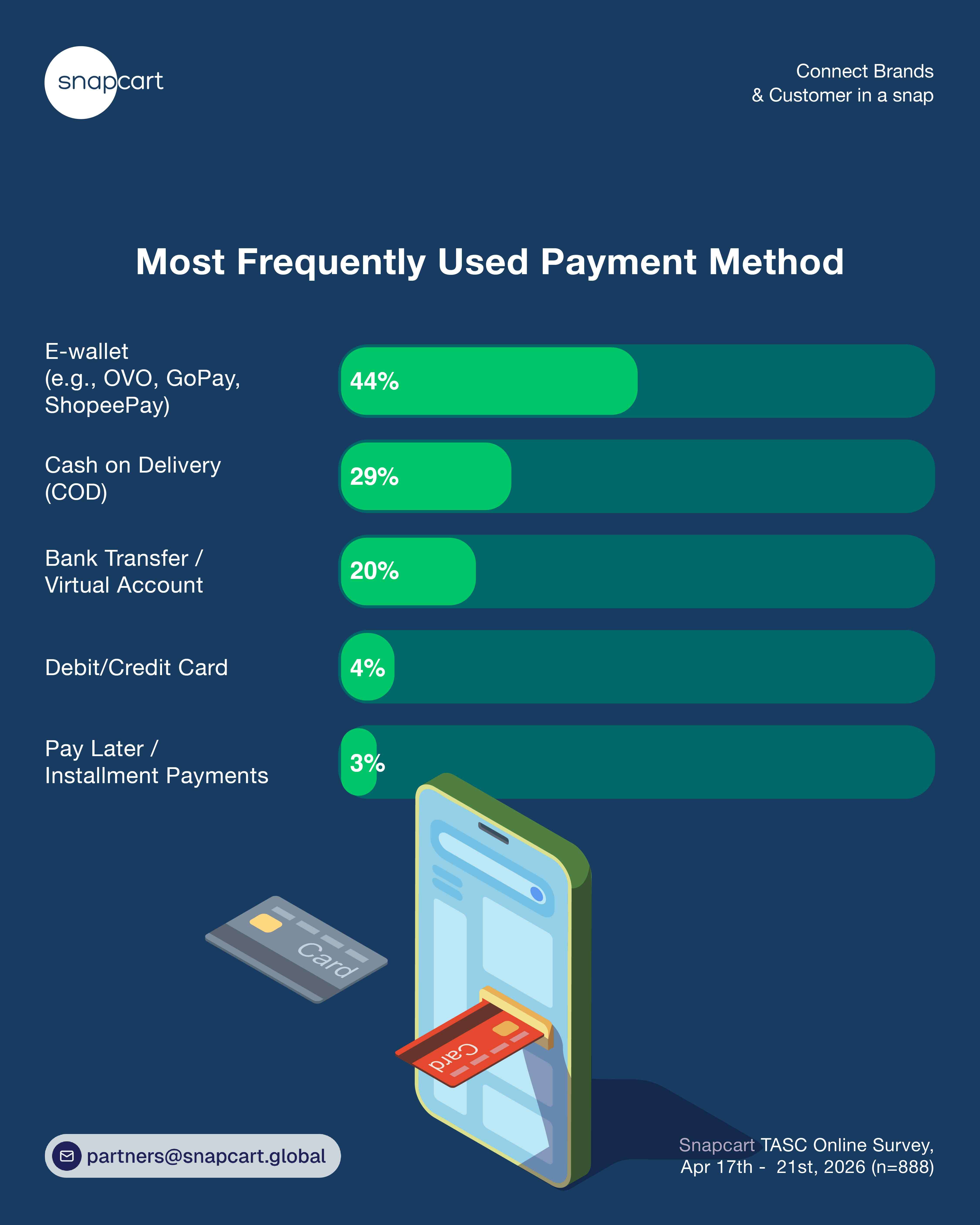

Digital Payments Lead, but COD Remains Important

The survey reveals that Indonesian consumers continue to use a diverse mix of payment methods.

E-wallets remain the most commonly used payment option, reflecting the growing adoption of digital financial services and marketplace-integrated payment ecosystems. At the same time, COD remains highly relevant, accounting for nearly one-third of respondents’ preferred payment method. This suggests that trust, spending control, and accessibility continue to influence payment decisions despite the growth of digital payments. Interestingly, PayLater usage remains relatively limited compared to other payment options, indicating that installment-based purchasing has not yet become a mainstream behavior among the surveyed consumers.

Shopping Habits Vary Across Age Groups

While platform leadership remains relatively consistent across age groups, the survey suggests that younger and older consumers exhibit different platform preferences. Shopee remains the most frequently used platform across all age segments, accounting for between 61% and 76% of primary platform usage. Its strongest position is observed among consumers aged 35–44 (76%), highlighting its broad appeal across mature consumer groups.

However, younger consumers demonstrate a stronger inclination toward TikTok Shop. Among respondents aged below 17 years old, 27% identify TikTok Shop as their most frequently used platform, compared to just 9% among consumers aged above 55 years old. This pattern suggests that social commerce continues to resonate more strongly with younger audiences, who are increasingly accustomed to discovering products through content, creators, and short-form videos.

Interestingly, Tokopedia shows relatively stronger preference among older consumers. While only 5% of consumers aged 17–34 identify Tokopedia as their primary platform, the figure rises to 15% among those aged 45–54 and 17% among consumers above 55 years old. The findings indicate that platform preference is becoming increasingly shaped by generational shopping habits, with younger consumers gravitating toward content-led commerce while older consumers continue to rely on more established marketplace ecosystems.

Younger Consumers Lead Digital Payment Adoption

Payment preferences also vary considerably by age. E-wallets remain the most frequently used payment method across all age groups, accounting for between 41% and 60% of primary payment usage. Adoption is particularly strong among younger consumers, reinforcing the growing role of digital financial services in everyday online shopping.

At the same time, COD (Cash on Delivery) demonstrates a clear age gradient. Among consumers aged below 17 years old, 40% prefer COD, while the figure declines steadily among older age groups, reaching 17% among consumers aged above 55 years old. Meanwhile, bank transfers become increasingly popular among adults aged 25–44, where approximately one in four consumers identify transfer or virtual account payments as their preferred method.

Although PayLater remains a niche payment option overall, adoption appears higher among consumers aged 35–54, suggesting that installment-based payments may currently resonate more with financially established shoppers than with younger consumers. These findings highlight that consumer payment behavior is not one-size-fits-all. As consumers progress through different life stages, their preferred payment methods evolve alongside their financial habits, trust levels, and purchasing needs.

Key Insights

1. Awareness Alone Is No Longer Sufficient

The survey reinforces that high awareness does not automatically translate into sustained usage. While most e-commerce platforms are widely recognized, only a few succeed in converting awareness into regular engagement and repeat usage. This highlights that acquisition alone is no longer enough, retention and habitual usage are becoming the key drivers of long-term platform success.

2. Consumer Preferences Are Increasingly Shaped by Age and Life Stage

Platform choice varies meaningfully across generations, indicating that e-commerce behavior is not uniform. Shopee maintains strong dominance across all age groups, particularly among consumers aged 35–44. Meanwhile, younger users show a stronger preference for TikTok Shop, reflecting their comfort with content-driven discovery. On the other hand, Tokopedia tends to perform relatively better among older consumers. This suggests that platform preference is increasingly shaped by generational habits where younger audiences gravitate toward social commerce, while older segments remain more aligned with established marketplace ecosystems.

3. Content-Led Commerce Is Becoming a Structural Advantage

TikTok Shop’s performance demonstrates the growing influence of content in driving purchase behavior. Its ability to combine entertainment, discovery, and transaction within a single experience has helped it convert awareness into active usage more effectively than many traditional marketplaces. For brands, this signals a shift: product discovery is no longer limited to search-based journeys, but increasingly embedded within content consumption.

4. Payment Behavior Is Highly Diverse

While e-wallets remain the dominant payment method overall, payment preferences vary significantly by age group. Younger consumers show stronger adoption of digital payment methods, while COD remains relatively more important among younger and lower-trust segments, declining steadily with age.

Bank transfers and virtual accounts are more commonly used among adults aged 25–44, while PayLater adoption though still niche is relatively higher among more financially established age groups. This indicates that payment strategy cannot be one-size-fits-all, and flexibility remains critical to reduce friction across different consumer segments.

5. Repeat Usage and Platform Stickiness Drive Competitive Advantage

As consumers increasingly concentrate their shopping activity on a single primary platform, the ability to drive repeat usage becomes more important than attracting first-time users. Leading platforms benefit not only from reach but from habit formation, convenience, and perceived value consistency. For brands, this reinforces the importance of loyalty-building mechanisms such as personalized offers, membership programs, retargeting, and post-purchase engagement to strengthen long-term retention.

Need to learn more about consumer habits and behavior? Contact us at partners@snapcart.global.